Impairment charges across Nigeria’s 10 banks surged to N3.2 trillion in their 2025 audited financial statements, as the end of regulatory forbearance triggered the sharp recognition of credit losses that had been deferred in earlier periods.

The increase represents a 39 percent jump from N2.3 trillion recorded in 2024, according to data compiled by BusinessDay.

The surge follows the Central Bank of Nigeria’s (CBN) decision to unwind Covid-era forbearance measures, which had allowed banks to restructure loans and delay classifying troubled exposures.

In practical terms, loans previously tagged as “performing” under forbearance have begun to migrate into Stage 3 (credit-impaired), driving a surge in provisioning under International Financial Reporting Standard (IFRS 9) rules.

Impairment captures a reduction in the value of a firm’s assets. It is otherwise captured as provision made for loan losses. Firms use impairments to write off worthless goodwill or report a reduction in goodwill.

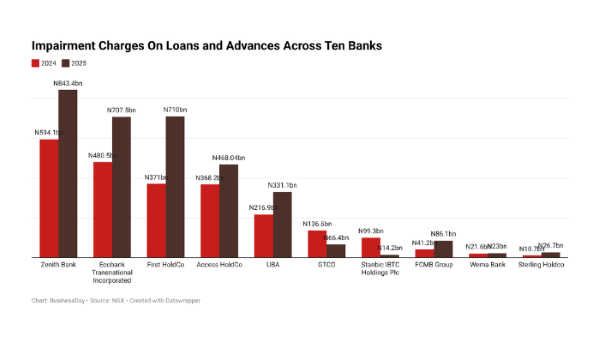

According to data tracked by BusinessDay, Zenith Bank led the impairment surge, with charges rising to N843.4 billion in 2025 from N594.1 billion in 2024. First HoldCo followed with impairments rising to N710 billion from N371 billion.

Ecobank Transnational Incorporated ranks third with impairment charges rising by 47 percent to N707.5 billion from N480.5 billion during the period reviewed.

Access HoldCo recorded provisions of N468.04 billion, up from N368.2 billion, while United Bank for Africa (UBA) saw impairments rise to N331.1 billion from N216.9 billion. FCMB Group rose to N41.2 billion from N86.1 billion.

Sterling Holdco also saw its loan impairment rise to N10.7 billion from N26.7 billion, and Wema Bank also rose to N21.6 billion from N23 billion.

On the other hand, GTCO and Stanbic IBTC Holdings Plc stood out as exceptions, with impairment charges declining to N66.4 billion from N136.6 billion and N14.2 billion from N99.3 billion, respectively, suggesting earlier recognition of problem loans before the end of forbearance.

Matilda Adefalujo, banking and fixed income analyst at Meristem Research, said Nigeria’s banking sector is undergoing a balance sheet reset as post-COVID regulatory relief unwinds, forcing lenders to recognise previously hidden risks and absorb higher loan losses.

She disclosed that during the pandemic, CBN allowed banks to restructure loans and delay stricter risk classification to cushion the economic shock. That support, however, masked the true quality of some assets and inflated capital ratios.

“With the regulator now ending forbearance, banks are reclassifying those loans and increasing provisions. What we are seeing is not necessarily a collapse in core earnings but the delayed recognition of credit risk.”

“Impairment charges surged across lenders in 2025, eroding profits despite still-solid operating income. Banks are effectively cleaning up their books after years of regulatory leniency,” the analyst added.

Nabila Mohammed, banking analyst at Chapel Hill Denham, during an interview, said the spike in impairments was largely driven by the reclassification of previously shielded loans.

According to her, credits that had benefited from regulatory relief were fully recognised once the forbearance window closed, forcing banks to take upfront provisions and reflect the true quality of their loan books.

“What we saw was a surge in impairment charges from H1 2025, as most banks had to exit regulatory forbearance and clean up their books,” she said.

These charges directly reduced the banks’ net income for the fiscal year, preventing them from distributing expected dividends to shareholders.

Collectively, the ten banks surveyed by BusinessDay reported a 10.4 percent decline in after-tax profit to N5.2 trillion in 2025 from N4.8 trillion reported in 2024.

Bad loans halt dividend payment for UBA, Access, FirstHoldco

Bad loans have forced major Nigerian lenders, including United Bank for Africa, Access Bank, and First HoldCo, to halt dividend payments for 2025, as a $2 billion (about N2.9 trillion) distressed exposure to Nestoil Limited triggers a sector-wide balance sheet reset, according to recent reports.

The latest banks hit by bad debts from Nestoil are United Bank of Africa (UBA) and Access Bank, which did not declare dividends for shareholders in their 2025 full-year financials. UBA’s full-year 2025 results showed loan loss provisions of N331 billion on its books, while Access Holdings’ charge for impairment on loans and advances to customers jumped 209 percent to N287.3 billion.

Available data show that Nigerian banks’ exposure to oil and gas at the end of 2024 was N21 trillion, with the major banks exposed to Nestoil being: UBA, First Bank of Nigeria (FBN), Access Bank Plc, FCMB Group, Union Bank, Ecobank and Afrexim Bank.

Under the “orthodox” and stringent leadership of CBN Governor Olayemi Cardoso, the regulator has prohibited affected banks from paying dividends for the 2025 financial year until they fully provision for these non-performing loans (NPLs).

The current bank loan crisis centres on Nestoil’s inability to service syndicated loans, which were facilitated during periods of higher oil production expectations. Nestoil is a large-scale indigenous operator.

“Nestoil’s inability to meet obligations has added to systemic banking pressure, particularly affecting lenders with high exposure to the independent oil and gas segment,” the report stated.

Apart from bad loan provisioning, the banks are also fighting to recover the debts owed to them.

In an interview with Arise TV, Oliver Alawuba, UBA’s CEO, said the bank’s 2025 performance was impacted by prudent and forward-looking risk management decisions, including loan loss provisions of N331 billion and fair value changes on derivatives amounting to N278 billion.

Alawuba confirmed that UBA is actively pursuing customers who have defaulted on their loans, aiming to restore the bank’s non-performing loan (NPL) ratios to levels that will support dividend distributions.

“We’re going after these defaulting customers, and there are signs that they are paying back. Once they do, we’ll be in a position to pay dividends for this year.”

NPLs are driving the cost of risk higher

Across the tier-one banks, the rise in impaired assets is feeding directly into higher provisioning, with a clear divergence in risk profiles when ranked by cost of risk. First HoldCo, where the cost of risk surged to 8.1 percent from 4.7 percent. Zenith Bank ranks next at 7.6 percent from 5.4 percent, indicating a steady but controlled deterioration in asset quality.

UBA, with the cost of risk rising to 4.7 percent from 3.6 percent, suggests a more moderate impact from NPL migration. GTCO at 4.9 percent, although this still represents a significant increase from 2.2 percent in 2024, and Access Holdings records the lowest cost of risk among peers at 4.1 percent in 2025, up from 2.5 percent in 2024.

NPLs rose to about 7 percent of total loans by early 2025, above the CBN’s 5 percent regulatory threshold. This arose because the payment obligations under the restructured loans had become due, and the loans could no longer qualify for special consideration as the forbearance period had ended.

In response to this, in a letter dated March 12, 2026, the CBN directed all Nigerian banks to restrict access to certain banking services to large-ticket obligors with NPLs.

The directive aims to strengthen the sufficiency of the credit framework, improve credit discipline, protect capital buffers, and thereby enhance the overall financial stability of the banking ecosystem.

Chinwe Michael is a financial inclusion advocate and economy journalist who uses compelling storytelling to drive awareness. With a background in Banking and Finance and experience across accounting, media, and education, she applies sharp analysis and attention to detail to every piece.