INTRODUCTION: The Central Bank of Nigeria began 2026 with measured optimism, delivering a 50-basis-point rate cut in February that reduced the Monetary Policy Rate to 26.5 per cent, the first move to stimulate growth in the economy. That decision according to CBN reflected eleven consecutive months of disinflation, with headline inflation easing to 15.06 per cent in February, food inflation falling sharply, and external reserves climbing to 13-year high of $50.45 billion.

However, just as the monetary easing was poised to support domestic demand and consolidate the recovery momentum, renewed geopolitical tensions introduced fresh external risks. The escalation of hostilities between the United States, Israel, and Iran in late February 2026 triggered the most significant global energy shock since the Russia-Ukraine war, exposing Nigeria’s economy to sudden cost pressures that risked eroding the benefits of the rate cut and complicating the CBN’s policy trajectory.

More fundamentally, while headline inflation declined in February 2026, it remains uncertain how the unfolding Middle East conflict will affect inflation data. Amid this, could Nigeria be on the verge of a recurrence of the 2022 inflationary pressure, when global supply shocks compelled apex banks worldwide into aggressive hawkish tightening even as post-pandemic recovery remained fragile? Against this backdrop, this brief explores Nigeria’s structural exposure to imported inflation, the channels through which external energy shocks transmit into domestic prices, the emerging monetary policy trade-offs facing the CBN, and the strategic policy considerations required to sustain macroeconomic stability in an increasingly volatile global environment.

2) Nigeria’s exposure to external energy cost pressures

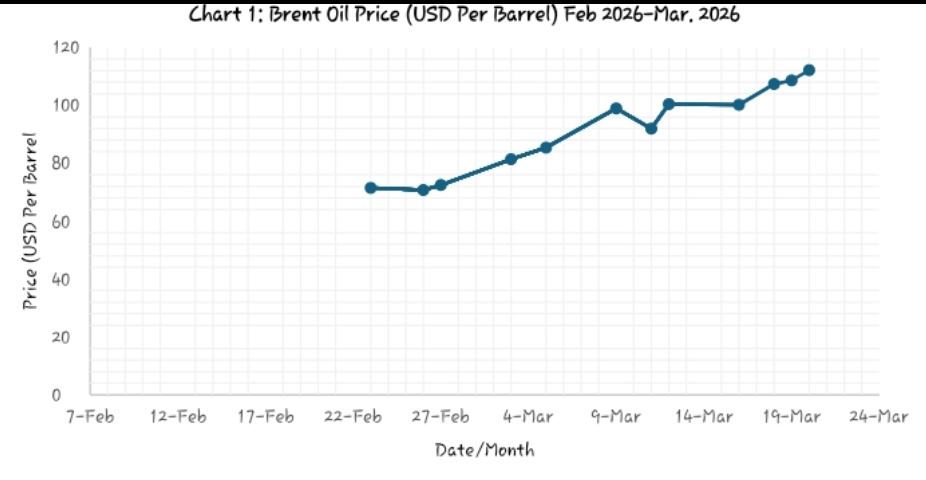

Nigeria’s vulnerability to external energy cost pressures results from the interaction between global crude oil price volatility and domestic structural constraints. Despite being one of Africa’s largest crude oil producers, the country remains heavily reliant on imported refined petroleum products due to decades of underinvestment in local refining capacity. Even with the Dangote Refinery producing substantial volumes of Premium Motor Spirit (PMS), Nigeria continued to import a significant portion of refined fuel as of late 2025, reflecting persistent gaps in domestic processing, logistical inefficiencies, and the legacy of deregulation coupled with undercapacity. Historical data revealed that petrol import bills rise sharply when global crude prices increase, a relationship that became evident over the years and also in early 2026 as disruptions in the Strait of Hormuz pushed Brent crude benchmarks from approximately $71 per barrel at the end of February to around $112 per barrel by the 20th of March. Domestic pump prices responded strongly, increasing by nearly 40 percent between late February and mid-March 2026, placing Nigeria among the countries with the largest global fuel price surges following the Middle East tensions.

In several regions, petrol prices reached N1,200-N1,300 per litre, with projections indicating potential increases to N1,500 per litre should the shock persist. This situation illustrates the paradox whereby higher crude export revenues enhance fiscal and foreign exchange inflows while simultaneously exerting upward pressure on domestic energy costs, indicating the economy’s structural exposure to external energy shocks.

3) Transmission mechanisms to domestic inflation

External energy cost pressures propagate into the Nigerian economy through multiple, mutually reinforcing channels. First, rising global crude prices transmit directly into domestic petrol prices, elevating transport, freight, and production costs across sectors heavily reliant on fuel. Following the removal of fuel subsidies in 2023, fluctuations in international oil prices pass directly into PMS prices without fiscal buffers, a dynamic further amplified by distribution and logistics costs, which constitute a substantial portion of the final price of goods and services. Second, higher costs for imported intermediate inputs increase production expenses for manufacturers, as Nigeria’s industrial sector relies extensively on imported machinery and components, whose landed costs rise with freight, insurance, and exchange rate pressures. Third, exchange rate movements can amplify domestic price pressures: heightened geopolitical risk may trigger capital outflows, weakening the naira and raising the local currency cost of imported goods. Collectively, these mechanisms facilitate the rapid transmission of global energy shocks into consumer prices, reducing household purchasing power and compressing corporate margins.

The CBN’s February 2026 rate cut aimed to stimulate growth after a prolonged tightening cycle. However, the sudden surge in global energy costs introduces a potential policy trade-off: maintaining an accommodative stance could amplify domestic price pressures, whereas tightening risks slowing recovery momentum.

This dilemma mirrors challenges faced by advanced central banks, including the European Central Bank and the U.S. Federal Reserve, which signaled caution amid energy-driven inflation spikes in early 2026. In Nigeria, structural vulnerabilities exposed during the 2022 Russia-Ukraine crisis exacerbate these risks.

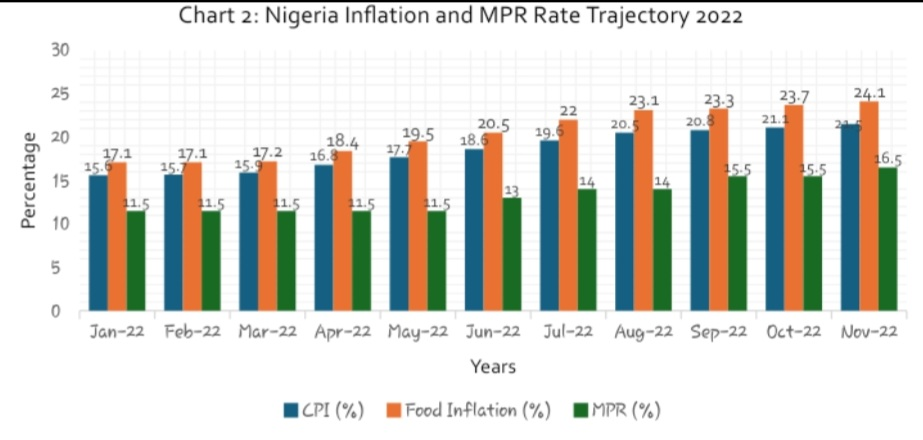

During that crisis, global monetary policy shifted rapidly toward hawkish tightening as energydriven inflation accelerated, with the U.S. Federal Reserve raising the federal funds rate from 0.25-0.50 per cent in early 2022 to 4.25-4.50 per cent by December 2022, the ECB lifting policy rates out of negative territory, and the Bank of England increasing the Bank Rate above 3.5 per cent. In emerging markets, the Central Bank of Nigeria raised the Monetary Policy Rate from 11.5 per cent in May 2022 to about 15.5 per cent by September 2022. This coordinated tightening response reflected the global imperative to anchor inflation expectations despite growth risks. Historical data from 2022 illustrate how energy price shocks can transmit into Nigeria’s inflation dynamics: annual headline inflation according to National Bureau of Statistics climbed from about 15.7 per cent in February 2022 to nearly 19.6 per cent by July and 20.5 per cent by August, coinciding with Brent crude prices that exceeded $120 per barrel amid the Russia-Ukraine conflict.

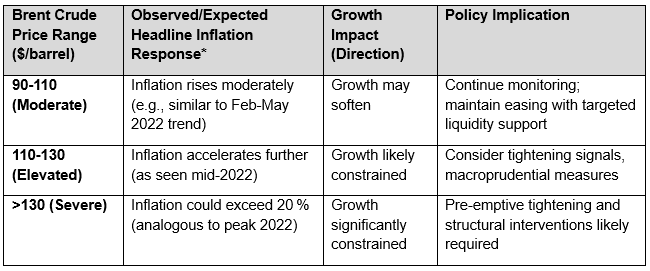

Table 1: Scenario outcomes based on energy price bands (Informed by 2022 Experience)

*Based on empirical evidence, in 2022, inflation climbed from midteens to approximately 19-20 per cent as Brent crude prices moved above $100-$120 per barrel amid supply shocks. This evidence-informed scenario highlights the narrow operational space confronting policymakers. Even under moderate energy price increases, there is historical precedent for inflation moving decisively upward, while severe price shocks have coincided with inflation breaching 20 per cent.

5) Strategic policy measures

At the start of the Russia war in Ukraine in 2022, Nigeria experienced rapid passthrough of global energy, supply chain-disruption and food shocks, with domestic inflation peaking above 18 %, transport and manufacturing costs soaring, and foreign exchange pressures intensifying (see chart 2: Nigeria inflation and MPR rate trajectory 2022).

The CBN refrained from implementing rate hikes, opting instead for targeted liquidity support to critical sectors and keeping the Monetary Policy Rate at 11.5 % from January to May. The first shift toward a more hawkish policy occurred in June 2022 (refer to chart 2). Concurrently, fiscal measures were directed towards conditional social support programs, rather than universal interventions.

Drawing from these insights, addressing the ongoing Middle East energy shock should involve robust reserve management and targeted short-term sectoral credit lines to stabilize essential supply chains.

Additionally, supporting at-risk households through direct cash transfers and advancing domestic refining and storage capacity are necessary to reduce reliance on imports. It is also crucial to continuously monitor the naira’s value and global commodity trends to safeguard against external shocks that could undermine the recent February rate cut and disrupt overall economic stability.

Prof. Joseph Nnanna is a Chief Economists at the Development Bank of Nigeria

Source: BusinessDay